If balance sheet does not balance double check your work. The four basic steps to developing a trial balance are.

How To Prepare A Correct Trial Balance Accounting Principles Youtube

The trial balance is prepared after all the transactions for the period have been journalized and posted to the General Ledger.

How to draw up a trial balance. Its always sorted by account number so anyone can easily scan down the report to find an account balance. The uses of the trial balance as follows. It has all the figures for the full year of trading.

Cash accounts receivables equipment bank loan. To see if the two totals are equal we draw up a trial balance at the end of an accounting period. How to draw up a Trial Balance from a list of T account balances part 2.

A trial balance mainly consists of 3 columns. Assets Expenses Drawings. Liabilities Revenue Owners Equity.

For each open ledger account total your debits and credits for the accounting period for which you are running the. Title the sum Total Liabilities and Owners Equity The balance sheet has been correctly prepared if Total Assets and Total Liabilities and Owners Equity are equal. Below is a list of all of our balances from our ledgers.

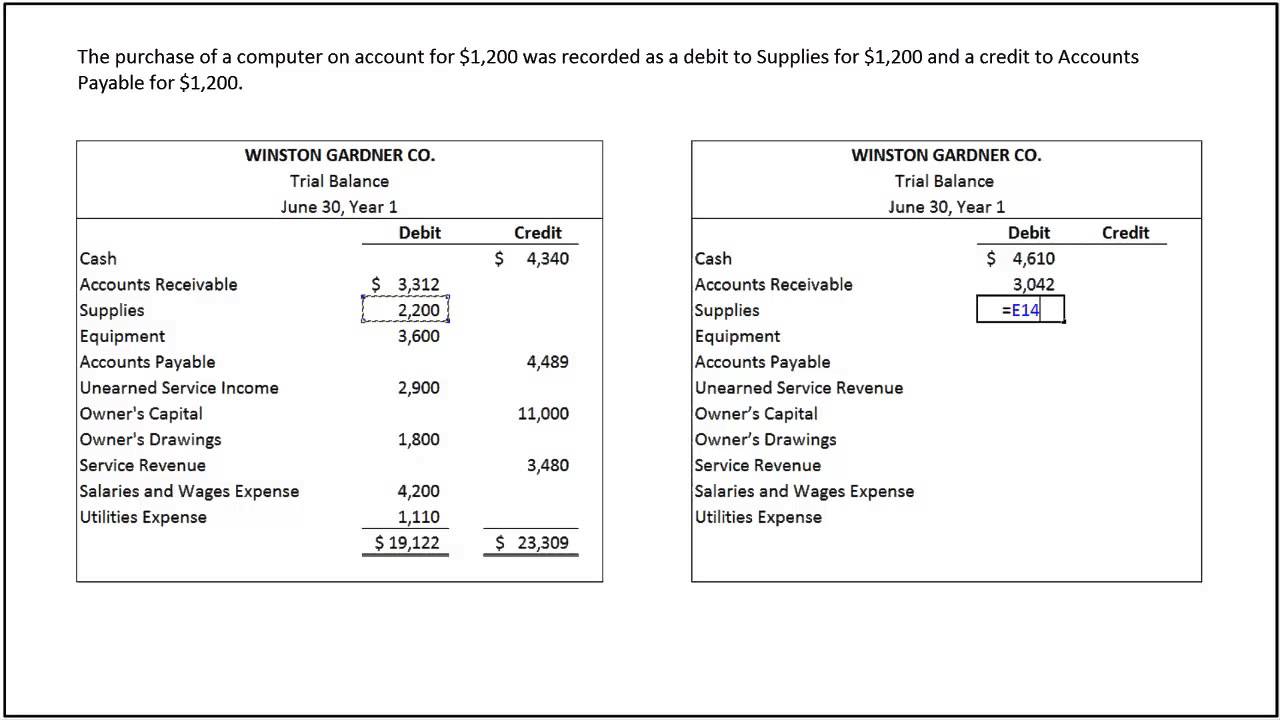

Column S does the same for every trial balance item copying the formula all the way down the column. Prepare a worksheet with three columns. Trial Balance is the report of accounting in which ending balances of different general ledger of the company are and is presented into the debitcredit column as per their balances where debit amounts are listed on the debit column and credit amounts are listed on the credit column and the total of both should be equal.

Trial Balance is a list of closing balances of ledger accounts on a certain date and is the first step towards the preparation of financial statements. In this example the formula CONCATENATE R30 O30 takes Restricted from R30 adds a space and then adds Property from O30. When the totals of the trial balance are equal we say that the trial balance totals agree.

Fill out the account name and. Total the debit and. What order are trial balance accounts in.

The account number should be the four-digit. Ledger balances are segregated into debit balances and credit balances. Both debit and credit totals are recorded in the trial balance.

Total Method and Balance Method. Then prepare a three column worksheet. Hstutorial Ledger Accounts and the Extraction of a Trial BalanceToday youre going to learn how to extract a trial balance from ledger entriesFirst youll.

Trial Balance Format The trial balance format is easy to read because of its clean layout. First of all we take all the balances from our ledgers and enter them into our trial balance table. Each row in the trial balance pertains to the information relating to an account.

In column 1 all the descriptions of individual ledger balances are recorded eg. How to Make a Trial Balance. According to the Total Method the sum of debits and credits of every account is shown in the trial balance ie.

The above trial balance example is for the end of the financial year. The format of the trial balance is a two-column schedule with all the debit balances listed in one column and all the credit balances listed in the other. How to draw up a Trial Balance from a list of T account balances part 2.

The heading for the trial balance is made up using details relating to name of the organisation and the instance to which the ledger account balances pertain. It provides a check on the accuracy of the ledger account balances - ensuring that entries have been made correctly. Remember the accounting equation.

It typically has four columns with the following descriptions. Column 3 is dedicated to the recording of all the credit ending balances. To prepare an income statement generate a trial balance report calculate your revenue determine the cost of goods sold calculate the gross margin include operating expenses calculate your income include income taxes calculate net income and lastly finalize your income statement with business details and the reporting period.

The debit column and credit column add up to the same total of 6403070 making the difference 000 - which means it is in balance. The trial balance is prepared with two different techniques. Account number name debit balance and credit balance.

Column 2 is the debit balances column where all the ending debit balances are recorded. Preparation of Trial Balance To prepare a trial balance we need the closing balances of all the ledger accounts and the cash book as well as the bank. One column is for account titles another is for debits and the other is for.

On the other hand according to the Balance Method only the Net balance which is the difference between credit and debit total is transferred and recorded. It is usually prepared at the end of an accounting period to assist in the drafting of financial statements. If this is the case then your balance sheet is now complete.

The header row consists of the labels for the information present in the trial balance. Do not prepare any. Trial balance for the Year End.

Steps for Preparing a Trial Balance List every open ledger account on your chart of accounts by account number. Fill in all the account titles and record their balances in the appropriate debit or credit columns. One column for the account name and the corresponding columns for debit and.